Fusion Microreactors & Distributed Energy Grids: 2026 Strategic Analysis for Investors, Utilities & Policymakers

A 4,000-word analyst-grade briefing on fusion microreactor technology, regulation, LCOE, geopolitics, and investment risk through 2040.

Fusion Microreactors for Distributed Energy Grids: A Strategic Analysis

April 2026

1. Summary

The 2022–2026 period has converted fusion energy from a perpetually-deferred scientific aspiration into a credible, capital-intensive infrastructure proposition with concrete commercial commitments. Cumulative private investment in fusion has reached approximately USD 9.77 billion across 53 companies, with USD 2.64 billion raised in the twelve months ending July 2025, the largest single-year increase since 2022 (Fusion Industry Association, 2025). Two private actors; Commonwealth Fusion Systems (CFS) and Helion Energy, have signed binding power purchase agreements (PPAs) with Google and Microsoft, respectively, anchoring grid-scale offtake commitments to the early 2030s and 2028.

Despite this momentum, the case for "fusion microreactors" as near-term distributed-grid assets remains preliminary. Most leading concepts are 100–500 MWe class machines positioned closer to traditional baseload than to truly modular distributed generation, and no concept has yet demonstrated net electrical output at scale. Levelized cost of electricity (LCOE) projections are widely contested, ranging from $50/MWh under aggressive Nth-of-a-kind assumptions to $150–200/MWh for first-of-a-kind plants, well above competing renewables plus-storage trajectories.

Strategic implications are threefold. First, regulatory clarity is consolidating in fusion's favor: the U.S. Nuclear Regulatory Commission (NRC) has elected to regulate fusion machines under its byproduct-materials framework (10 CFR Part 30) rather than as utilization facilities under Parts 50/52/53, materially reducing licensing risk. Second, supply-chain dependencies; particularly tritium and lithium-6, create strategic bottlenecks that warrant national-security-grade attention. Third, the commercialization race is now bipolar: U.S. private capital and Chinese state-directed infrastructure investment dominate, with Europe at risk of strategic marginalization absent the EU Fusion Strategy expected in 2026.

2. Introduction & Context

Fusion energy occupies an unusual position in the contemporary energy transition: simultaneously a long-duration scientific quest and an emerging asset class. Three convergent forces explain why fusion microreactors are now a topic of executive-level interest.

First, electricity demand is structurally accelerating. The International Energy Agency's World Energy Outlook 2025 characterizes the current era as the "Age of Electricity," projecting roughly 40% growth in global electricity demand within a decade, driven primarily by AI workloads, data-center buildout, electrification of transport and industry, and reshoring of manufacturing. In the United States alone, hyperscale data-center expansion is projected to require over 100 GW of incremental capacity. This demand pull has rendered hyperscalers (Microsoft, Google, Amazon, Meta, Oracle) into active counterparties for firm, low-carbon power, prepared to underwrite first-of-a-kind energy technologies.

Second, scientific breakthroughs since 2021 have shifted the credibility frontier. The National Ignition Facility (NIF) at Lawrence Livermore National Laboratory achieved scientific energy breakeven (Q > 1) in December 2022 and has reproduced higher-yield ignition events on at least nine subsequent occasions. The Joint European Torus (JET) produced 59 megajoules of fusion energy in a single shot in 2021. Tokamak Energy's ST40 reached ion temperatures of 100 million °C in 2022, the first private spherical tokamak to do so. These results compress the perceived gap between physics demonstration and engineering deployment.

Third, the strategic backdrop; energy security after the 2022 European gas crisis, decarbonization commitments, and intensifying U.S./China technology competition, has elevated fusion from a basic-science line item to a stated national-security priority across multiple jurisdictions. The phrase "fusion microreactor" remains imprecisely defined. In contemporary industry usage it generally connotes compact, factory-fabricable, sub-500 MWe machines, as distinct from gigawatt-class tokamaks such as ITER. Whether such machines will genuinely operate as distributed (sub-50 MWe, behind-the-meter) assets, or whether grid-scale (100–500 MWe) deployments will dominate, is itself contested.

3. Technology Readiness & Key Players

3.1 A Note on TRL Frameworks for Fusion

The IAEA's 2024 publication Considerations of Technology Readiness Levels for Fusion Technology Components applies the standard 1–9 NASA-derived TRL scale to fusion subsystems but emphasizes that integrated TRL assessment for a complete fusion power plant remains at TRL 3–4 across all concepts. Subsystems vary widely: tokamak plasma confinement physics is at high TRL for short-pulse experimental conditions but at low TRL for steady-state, neutron-irradiated reactor operation. Tungsten plasma-facing materials, for example, are TRL 9 in JET-class experimental conditions but only TRL 3 for a DEMO-class fusion power plant (UKAEA, 2021). TRL claims advanced by individual companies should therefore be interpreted with caution; they typically refer to specific subsystems rather than the integrated plant.

3.2 Major Private and Public Actors

Callout: Selected Funding Snapshot (mid-2025)

• Commonwealth Fusion Systems: ~$3.0 B cumulative (incl. $863 M Series B2, August 2025)

• Helion Energy: ~$1.0 B cumulative (incl. $425 M Series F, January 2025; $5.4 B valuation)

• TAE Technologies: ~$1.3 B cumulative

• Tokamak Energy: $335 M cumulative ($275 M private + $60 M U.S./UK governments)

• General Fusion: ~$440 M cumulative; under acute funding pressure as of mid-2025

• Pacific Fusion: $900 M Series A (Nov 2024) Sources: Company disclosures; Fusion Industry Association (2025)

Commonwealth Fusion Systems (CFS) – High-field compact tokamak. CFS is constructing SPARC, a high-temperature superconducting (HTS) tokamak in Devens, Massachusetts, with f irst plasma scheduled for 2026 and a net-energy demonstration target of 2027. Its commercial follow-on, ARC, is a 400 MWe plant planned for the James River Industrial Center in Chesterfield County, Virginia, in collaboration with Dominion Energy and a 200 MW PPA with Google. CFS has raised approximately one-third of all global private fusion capital. Integrated plant TRL: 4 (subsystems: HTS magnets demonstrated at TRL 5–6 following the 2021 toroidal f ield model coil test).

Helion Energy – Pulsed field-reversed configuration (FRC) with direct energy conversion. Helion's seventh-generation prototype, Polaris, began operations in late 2024. In January 2026 the company reported the first deuterium-tritium (D-T) operation by a privately funded fusion device, achieving plasma temperatures of approximately 150 million °C (~13 keV). Helion's commercial reactor in Malaga, Washington, is contractually obligated to deliver at least 50 MW to Microsoft by 2028 (with Constellation Energy as power marketer). This timeline has, by independent observers, including the Fusion Industry Association's CEO, have described as "ambitious." Integrated plant TRL: 3–4.

TAE Technologies – Advanced beam-driven FRC, hydrogen-boron (p-¹¹B) fuel cycle. In November 2025, TAE reported the first FRC plasma formed exclusively via neutral-beam injection (Norm device). The company subsequently announced it would skip its previously planned sixth-generation Copernicus device and proceed directly to its first power-plant prototype, Da Vinci, targeting early-2030s operation. Aneutronic p-¹¹B reduces neutron damage and tritium handling burdens but operates at higher required ion temperatures (~3 billion °C). Integrated plant TRL: 3.

Tokamak Energy – Compact spherical tokamak with HTS magnets. ST40 demonstrated 100 million °C ion temperatures in 2022, validated in peer-reviewed work in Nuclear Fusion (Tokamak Energy and the ST40 Team, 2024). A $52 million tripartite ST40 upgrade was announced in December 2024 with the U.S. DOE and the UK's DESNZ. The company is one of eight U.S. DOE Milestone-Based Fusion Development Program awardees. Integrated plant TRL: 3–4.

General Fusion – Magnetized target fusion (MTF). General Fusion's LM26 demonstration achieved first plasma in February 2025 and successful lithium-liner compression in April 2025. However, in May 2025 the company disclosed "unexpected and urgent financing constraints," conducted a ~25% workforce reduction, and announced openness to strategic alternatives including sale. A $22 million bridge round closed in mid-2025. Integrated plant TRL: 3.

Other notable private actors. Pacific Fusion (laser-based; emerged from stealth November 2024 with a $900 M Series A); Proxima Fusion (Germany; €130 M for a quasi-isodynamic stellarator); Marvel Fusion (Germany; €113 M Series B for laser inertial); Type One Energy (stellarator, Tennessee); Zap Energy (sheared-flow Z-pinch); First Light Fusion (projectile-driven inertial); and Energy Singularity (China; HTS tokamak).

3.3 National Programs

• United States. DOE Office of Fusion Energy Sciences operates a roughly USD 790 million annual program (FY2024 appropriation) plus NNSA's USD 690 million inertial confinement portfolio. The Milestone-Based Fusion Development Program selected eight private awardees in 2023; the Fusion Innovation Research Engine (FIRE) Collaboratives commit USD 107–180 million.

• China. EAST tokamak set a record in 2025 for sustained plasma >100 million °C for over 1,000 seconds. The BEST (Burning Plasma Experimental Superconducting Tokamak) facility in Hefei targets first plasma in 2027. The Comprehensive Research Facility for Fusion Technology (CRAFT) campus is reported in open sources at ~USD 570–700 million. The China Fusion Engineering Test Reactor (CFETR) targets 200–1,000 MW fusion power. A 2024 Chinese Academy of Engineering report set a strategic target of "commercial energy supply by 2040." China's national fusion appropriation is widely reported as roughly twice the U.S. level, though precise figures are not publicly verified.

• European Union. ITER first plasma was rescheduled in July 2024 to the mid-2030s, with deuterium-tritium operations now targeted for 2039. The European Commission has proposed €222 million for fusion within the 2026–2027 Euratom Work Programme and is preparing the EU's first-ever Fusion Strategy, responding directly to the Draghi competitiveness report.

• United Kingdom. The Spherical Tokamak for Energy Production (STEP) program at West Burton received a £2.5 billion commitment, targeting an industrial prototype around 2040. The UK was the first jurisdiction to enact fusion-specific regulation distinguishing it from fission.

• India. The Institute for Plasma Research operates the SST-1 superconducting tokamak; SST-2 (a low-fusion-gain DEMO precursor of ~100–300 MW) is targeted for the late 2020s/early 2030s. India remains an ITER full partner and provides the cryostat in-kind contribution.

4. Grid Integration Considerations

Even if fusion devices reach net-electrical output on schedule, integration into modern distribution networks introduces a distinct engineering risk layer that has received limited rigorous public analysis.

Pulsed versus steady-state output. A fundamental design distinction divides the field. Tokamak-class machines (CFS, Tokamak Energy) and stellarators target long-pulse or steady state operation similar to existing thermal plants, producing heat that drives a Rankine cycle. Pulsed concepts (Helion, General Fusion, inertial fusion) produce energy in discrete shots; Helion's Polaris currently fires roughly every ten minutes; commercial operation requires sub second pulse repetition. Pulsed direct-conversion architectures (Helion) bypass the steam cycle entirely, recovering electricity via induced currents. Pulsed operation imposes severe demands on power conditioning, capacitor banks, and grid-side filtering to deliver smoothed AC output to interconnections.

Load-following and firm capacity role. The classic "baseload" framing is increasingly out of style. As variable renewable energy (VRE) penetration rises, system operators require dispatchable, flexible firm capacity. The 2021 National Academies report Bringing Fusion to the U.S. Grid explicitly framed pilot-plant requirements around providing "firm and dispatchable" power complementing renewables, not against them. A 2025 preprint analyzing fusion renewable integration similarly concluded that fusion's strategic value is "not as a standalone baseload power source, but as a flexible, integrated partner to renewables" (Bragg-Sitton et al., as cited in cloudfront preprint). However, fusion plants are highly capital-intensive and operationally favor high capacity-factor utilization; whether they can economically load-follow remains an open question.

Grid-forming inverters and islanding. For genuinely distributed deployment, particularly fusion microreactors co-located with data centers, industrial loads, or remote communities, grid-forming (GFM) inverter technology is essential. GFM inverters synthesize voltage and frequency references rather than passively following them, enabling black-start, fault ride through, and seamless islanding (Watson et al., 2020; MDPI Energies, 2022). The maturity of GFM controls in renewable microgrids is improving rapidly, but their integration with pulsed, high-current fusion power conversion systems is essentially unstudied in peer-reviewed literature. The National Academies report explicitly noted that "fusion has generic properties such as on-site fuel, baseload capability, and potentially dispatchable that are attractive to blackstart" but flagged the absence of design-specific studies.

Thermal output management. Tokamak/stellarator concepts produce high-grade heat that could be directed to district heating, hydrogen electrolysis, or industrial process heat. However, structural materials such as Eurofer reduced-activation ferritic-martensitic (RAFM) steel limit outlet temperatures, constraining downstream applications, particularly high-temperature electrolysis and cement/steel decarbonization use cases.

Interconnection scale mismatch. A 400 MWe ARC plant interconnecting at distribution voltage is implausible; such facilities will require transmission-level interconnection, similar to current nuclear plants. Behind-the-meter deployments at hyperscale data centers (where parcel-scale demand may approach 500–1,000 MW) may circumvent transmission-queue bottlenecks, an attribute already cited as a key factor in the CFS/Google and Helion/Microsoft PPAs.

5. Regulatory & Licensing Landscape

5.1 United States: NRC Part 30 vs. Parts 50/52/53

The U.S. regulatory pathway for fusion has clarified materially in the last 36 months. The Nuclear Energy Innovation and Modernization Act (NEIMA, P.L. 115-439, enacted January 2019) directed the NRC to establish a fusion regulatory framework by December 31, 2027.

In SECY-23-0001 (January 2023), NRC staff outlined three options:

- Regulate fusion as a utilization facility under 10 CFR Parts 50/52 or the new Part 53 risk informed framework (analogous to fission reactors);

- Regulate fusion as a byproduct-materials facility under 10 CFR Part 30 (analogous to particle accelerators); or

- A hybrid pathway with risk-based decision criteria.

On April 13, 2023, the Commission unanimously selected Option 2 via Staff Requirements Memorandum SRM-SECY-23-0001. The 2024 ADVANCE Act subsequently codified that radioactive materials produced by a fusion machine fall within the Atomic Energy Act's definition of byproduct material, creating a statutory anchor.

On February 26, 2026, the NRC issued a proposed rule implementing this framework, with a 90 day comment period through May 27, 2026, and a final rule targeted for October 2026. The rule introduces formal definitions of "fusion machine" and updates Part 30 byproduct-material rules; it also accommodates Agreement States, which currently regulate research-scale fusion devices and have already issued the first state-level commercial fusion materials licenses (e.g., Tennessee Department of Environment and Conservation for Type One Energy's stellarator test bed; Washington State Department of Health Large Broad Scope license for Helion)

Strategic implication: The Part 30 election is materially favorable to private developers. It is performance-based, technology-inclusive, less prescriptive than reactor licensing, and significantly reduces project-finance risk. The Fusion Industry Association notes this would make the U.S. the second jurisdiction (after the UK) to establish a fusion-specific regulatory regime. However, several gaps remain unresolved: fee structures, 10 CFR Part 61 waste classification updates for novel fusion activation products, and a separate framework for mass manufactured fusion machines (relevant to genuinely distributed microreactor deployment).

5.2 IAEA Guidance

The IAEA's World Fusion Outlook (first edition 2023; third edition 2025) explicitly states that existing IAEA safety standards developed for fission; principally SSR-2/1 (Safety of Nuclear Power Plants: Design) and SSG-2 (Deterministic Safety Analysis) are not directly applicable to fusion installations. The IAEA convened the inaugural World Fusion Energy Group in 2024 to develop fusion-specific definitions, characteristics, and harmonized criteria. The IAEA's 2024 publication on TRLs for fusion components provides the first formal multilateral TRL methodology for the sector.

5.3 European Union: Euratom Treaty Considerations

The Euratom Treaty (1957) governs nuclear research, safety, and safeguards across the EU. Fusion's classification under Euratom is currently inherited from fission frameworks, an alignment widely criticized as ill-suited to fusion's distinct hazard profile. The EU Fusion Strategy expected in 2026, the GO4Fusion public-private partnership pilot (€75 M through 2027), and the planned €222 million fusion-related allocation in the 2026–2027 Euratom Work Programme are intended to address this gap. The Clean Air Task Force and European Parliament fusion industry coalition have publicly called for a "fit-for-purpose regulatory framework that clearly distinguishes fusion energy from fission energy" (CATF, November 2025).

5.4 DOE Bold Decadal Vision (2022–2024)

Announced at the March 17, 2022, White House Summit, the Bold Decadal Vision for Commercial Fusion Energy established three strategic objectives: (i) demonstrate an operating fusion pilot plant in the 2030s; (ii) prepare commercial deployment scale-up; and (iii) ensure equitable deployment. Implementation has included the Milestone-Based Fusion Development Program (eight awardees, contracts signed June 2024); the FIRE Collaboratives (USD 107 million awarded January 2025); INFUSE public-private vouchers; and the DOE Fusion Energy Strategy 2024 released in June 2024. The Fusion Industry Association has publicly argued that delivery on the Vision requires a one-time supplemental appropriation of approximately USD 3 billion, a level not yet enacted.

6. Economic Viability & Investment Signals

6.1 LCOE Projections - Estimates Vary Significantly

LCOE estimates for fusion span more than a 4× range and should be treated with caution; no commercial fusion plant has yet operated, and "estimates vary significantly across sources."

| Source / Concept | LCOE Estimate | Notes |

|---|---|---|

| Inertial fusion (Royal Society Phil. Trans. A, 2020) | ~$80/MWh | Earlier ICF cost analysis |

| First Light Fusion (revised design) | Comparable to renewables | Lower-frequency ~60-second pulse design |

| Assystem (UK), 2021 | £60–£100/MWh | Standard build with learning |

| Wade (ARIES tradition), as cited in arXiv 2101.09150 | ~$50/MWh “sweet spot”; up to ~$100/MWh | Nth-of-a-kind commercial assumptions |

| Industry consensus (NOAK) | $60–$100/MWh | Optimistic learning-curve assumption |

| First-of-a-kind plants (independent analysis) | $150–$200/MWh | Reflects FOAK risk premium |

| Helion (company claim) | ~$10/MWh | Not independently validated |

For comparison: SMR fission projections, $40–$60/MWh; utility-scale solar-plus-storage (BloombergNEF), $35–$45/MWh by 2030; offshore wind, ~$50/MWh; gas with CCS, ~$70 $90/MWh assuming a $100/tonne carbon price.

Costing methodology has improved. ARPA-E commissioned cost-frameworks (Woodruff Scientific, 2017–2024) and the open-source pyFECONs codebase, aligned with IAEA (2001), Gen-IV EMWG (2007), and EPRI (2024) chart-of-accounts standards, provide the first auditable, traceable LCOE methodology for fusion (Woodruff et al., arXiv 2601.21724; Clean Air Task Force International Working Group, 2024–2025). Until first-of-a-kind plants operate, however, LCOE remains a paper exercise.

6.2 Capex/Opex Considerations

Major capex drivers vary by concept: HTS magnets and cryogenic plant for tokamaks (CFS, Tokamak Energy); high-energy lasers for inertial concepts; pulsed power supplies and capacitor banks for FRC/MTF. Tritium fuel-cycle systems, breeding blankets, divertors, and remote handling equipment represent substantial cost categories largely absent from existing experimental machines and contributing significantly to FOAK uncertainty.

6.3 Investment Trends

The Fusion Industry Association's Global Fusion Industry in 2025 report records:

• Cumulative private + public funding: USD 9.7 billion (53 companies)

• 12-month inflow (Jul 2024 – Jul 2025): USD 2.64 billion (+178% vs. prior year)

• Public-source funding: ~USD 800 million cumulative (+84% YoY)

• Direct fusion employment: 4,607 people (+~4× since 2021); ~9,300 supply-chain jobs

• Companies' self-reported additional capital required to first pilot plant: median $700 M; aggregate $77 billion (~8× capital committed to date)

Notable deals: Pacific Fusion ($900 M Series A, Nov 2024); CFS ($863 M Series B2, Aug 2025); Helion ($425 M Series F, Jan 2025); Marvel Fusion (€113 M Series B); Proxima Fusion (€130 M); TAE Technologies (~$150 M, 2025). Investor diversification has expanded materially: technology venture (DCVC, Breakthrough Energy Ventures, Khosla, Galaxy Interactive), industrial strategics (Eni, Equinor, Chevron, Siemens Energy, Nucor), sovereign and quasi-sovereign capital (Temasek, In-Q-Tel, EIC Fund), and hyperscaler corporate development (Google, Microsoft via partnerships).

Comparison to SMRs. Advanced fission investment surged in parallel during 2025—TerraPower ($650 M Series C), X-energy ($700 M Series C-1), Radiant ($300+ million), Last Energy ($100+ million)—with SMRs and microreactors capturing roughly 75% of nuclear-fission private equity activity. SMRs benefit from regulatory precedent and supply-chain inheritance from existing nuclear; fusion benefits from a more permissive licensing pathway but lacks operational reference plants.

Callout: A Caution on Hyperscaler PPAs: The CFS–Google (200 MW, ~early-2030s, ARC) and Helion–Microsoft (≥50 MW, 2028, Polaris-class commercial reactor) PPAs are widely cited as commercial validation. They are genuinely significant—the first private commercial fusion offtake agreements—but contain conditional structures: Microsoft's contract uses Constellation Energy as power marketer with backstop sourcing, and timelines remain widely viewed by independent observers as ambitious. Investors should treat PPA announcements as call options on technical success, not as evidence of technical maturity.

7. Geopolitical & Energy Security Dimensions

7.1 Race to Commercialization

As of end-2025, of approximately €13 billion in cumulative fusion finance: €6.9 billion (≈53%) flows to ~42 U.S. companies, €4.4 billion (≈34%) to ~8 Chinese companies, and €712 million (<5%) to ~8 European companies (Science|Business, January 2026, citing FIA data). The U.S. model emphasizes private capital and milestone-based public co-funding; the Chinese model emphasizes state-directed infrastructure (CRAFT, BEST, CFETR) backed by China Fusion Energy, a 2024-formed industrial consortium of 25 state-owned enterprises, four universities, and key private firms.

The Special Competitive Studies Project (SCSP) 2025 report Fusion Power: Enabling 21st Century American Dominance documents that China filed more fusion-related patents than the United States in 2023 and produces approximately ten times as many fusion-relevant Ph.D. graduates annually. These metrics warrant interpretive caution—patent quantity does not equal quality, and Ph.D. counts conflate plasma physics with adjacent disciplines—but they are consistent with directional concerns expressed in DOE and bipartisan Congressional commission reporting.

7.2 Supply Chain Dependencies

Tritium. Global commercial tritium stockpiles are estimated at approximately 25 kilograms, sourced primarily from 19 Canadian CANDU reactors producing ~0.5 kg/year each as a moderator byproduct (Pearson, Kyoto Fusioneering, 2022; Science, 2022). Half of the CANDU fleet is scheduled to retire this decade. ITER's 2018 research plan projects the global tritium inventory peaking before 2030, then declining. Fusion's tritium fuel cycle is therefore not yet self-sufficient at industrial scale, and demonstrated tritium-breeding blankets achieving tritium breeding ratios (TBR) >1 remain at low TRL. ARC-class designs assuming FLiBe blankets (lithium fluoride + beryllium fluoride) and STEP-class designs assuming liquid lithium are credible on paper but unverified in operation. Aneutronic concepts (TAE p-¹¹B; Helion D-³He) sidestep tritium but introduce other constraints (helium-3 scarcity for Helion; very-high temperature requirements for TAE).

Lithium-6. Tritium breeding requires lithium-6 enrichment to typically 30–90%. The natural abundance of ⁶Li is 7.5%. Commercial supply of enriched lithium-6 is effectively zero: the historical U.S. COLEX (mercury-amalgam) process was shut down in the 1960s on environmental grounds, and current limited supply derives from legacy stockpiles or research scale facilities. A viable lithium-6 supply route is identified as a critical-path challenge for the European DEMO program (Giegerich et al., Fusion Engineering and Design, 2019). This is a strategic chokepoint analogous to the rare-earth dependencies that have shaped recent industrial policy.

Beryllium. A single beryllium-multiplier blanket fusion reactor would require approximately the global annual beryllium supply (Bradshaw et al., 2011; Pearson 2020). Lead-lithium and FLiBe blanket alternatives reduce but do not eliminate beryllium dependence.

Deuterium. In contrast, deuterium is essentially unconstrained: roughly 1 in 6,500 hydrogen atoms in seawater is deuterium, an effectively inexhaustible resource.

HTS materials and rare earths. REBCO (rare-earth barium copper oxide) high-temperature superconductor tape is critical to compact tokamak designs (CFS, Tokamak Energy). Production capacity is concentrated in a small number of suppliers in the United States, Japan, and Europe. The Fusion Industry Association's 2025 Supply Chain Report finds that 31% of fusion companies are concerned about precision-engineering supplier availability for current commercial needs, rising to 63% for future needs.

7.3 Strategic Posture Implications

Fusion microreactors, if technically realized, would materially reshape energy geopolitics by:

• Reducing dependency on imported hydrocarbons and lithium-ion battery supply chains;

• Creating new strategic chokepoints around tritium, lithium-6, beryllium, and HTS;

• Providing forward-deployable firm power (relevant to military bases, remote-grid resilience, disaster recovery)

• Enabling "energy sovereignty" framings that may complicate non-proliferation regimes despite fusion's substantially lower proliferation risk relative to fission.

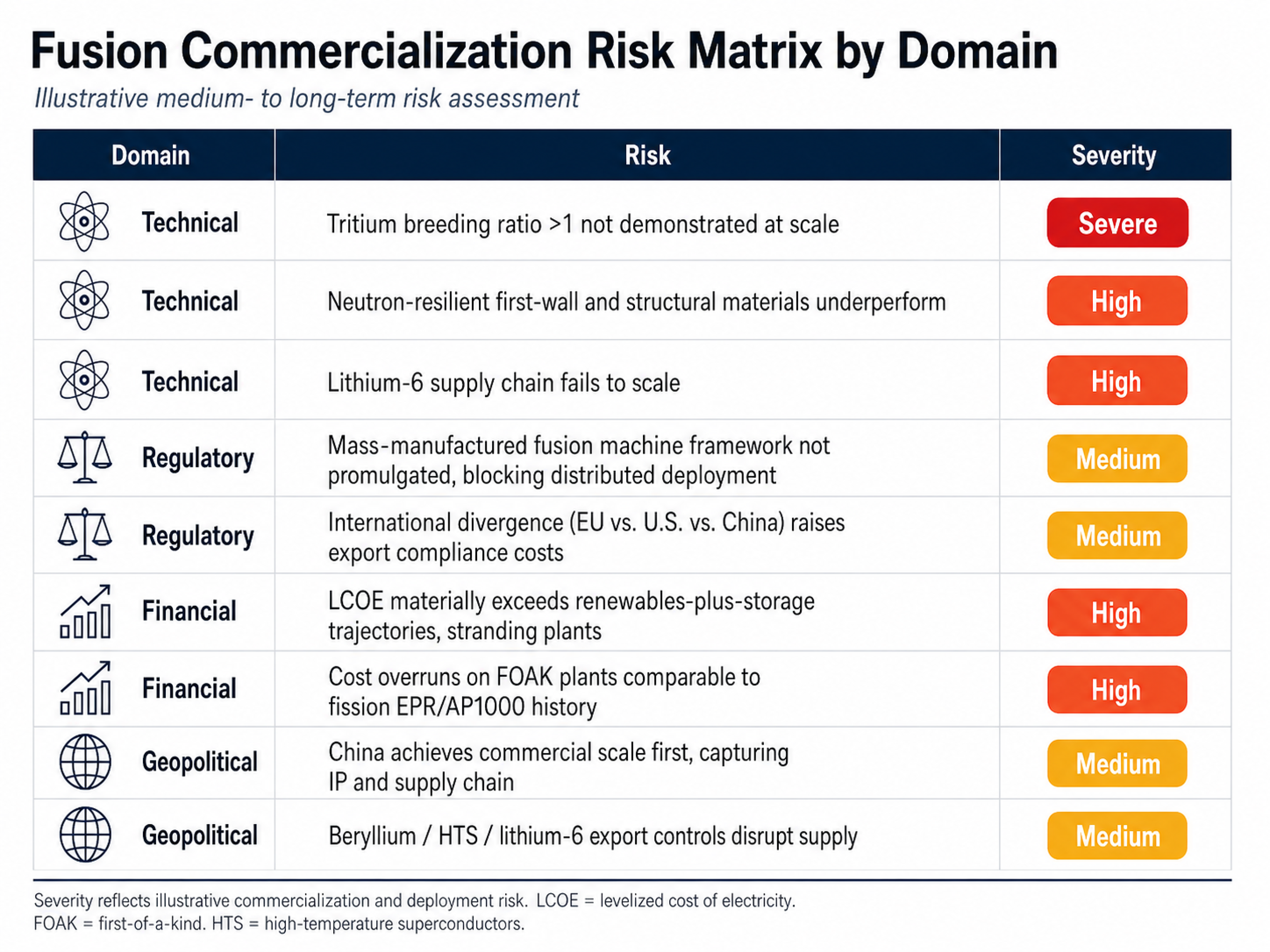

8. Risk Matrix

Risks below are ranked Low / Medium / High / Severe based on a synthesis of National Academies (2021), FIA (2024, 2025), CRS R48866, and IAEA World Fusion Outlook (2023, 2025) findings. Preliminary findings indicate the medium-term horizon (2030–2040) is the most acute risk window.

| Domain | Risk | Severity |

|---|---|---|

| Technical | Failure to demonstrate net electrical (Q > 1) at any private device | High |

| Technical | Pulsed-to-continuous-output power conditioning challenges (Helion-class) | Medium |

| Regulatory | NRC final rule (Oct 2026) could face procedural delays | Low |

| Regulatory | Agreement State capacity to license commercial-scale fusion | Medium |

| Financial | Capital intensity outpaces investor appetite; consolidation accelerates | High |

| Financial | Hyperscaler PPA milestones missed, eroding investor confidence | Medium |

| Sociopolitical | Public conflation of fusion with fission limits siting | Medium |

Short Term: 2025–2030

| Domain | Risk | Severity |

|---|---|---|

| Technical | Tritium breeding ratio > 1 not demonstrated at scale | Severe |

| Technical | Neutron-resilient first-wall and structural materials underperform | High |

| Technical | Lithium-6 supply chain fails to scale | High |

| Regulatory | Mass-manufactured fusion framework not promulgated | Medium |

| Regulatory | International divergence raises compliance costs | Medium |

| Financial | LCOE exceeds renewables-plus-storage, stranding plants | High |

| Financial | FOAK cost overruns comparable to fission history | High |

| Geopolitical | China achieves commercial scale first, capturing supply chain | Medium |

| Geopolitical | Export controls (beryllium, HTS, lithium-6) disrupt supply | Medium |

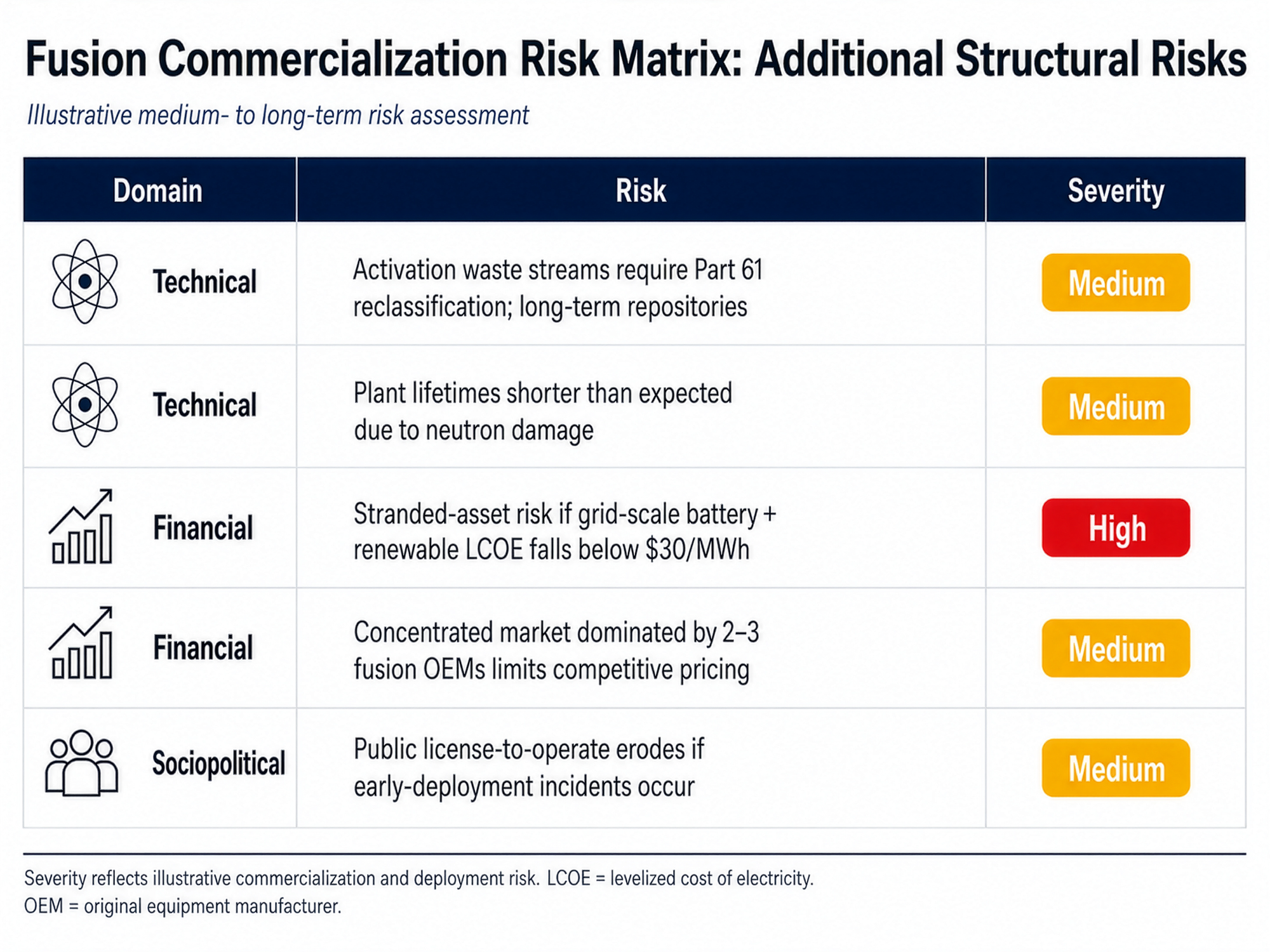

Medium Term: 2030–2040

| Domain | Risk | Severity |

|---|---|---|

| Technical | Activation waste requires new classification and repositories | Medium |

| Technical | Plant lifetimes shorter than expected due to neutron damage | Medium |

| Financial | Stranded assets if renewables plus storage < $30/MWh | High |

| Financial | Market concentration limits competitive pricing | Medium |

| Sociopolitical | Loss of public license-to-operate after incidents | Medium |

Long Term: 2040+

Caveat. Severity ratings are analytical judgments synthesized from cited literature, not quantitative probability estimates. Subject to further validation as net-electrical demonstrations succeed or fail through 2027–2030

9. Strategic Recommendations

9.1 For Energy Utilities

- Adopt a real-options posture, not a procurement posture. Treat fusion engagement as call-option positioning—via low-cost MOUs, site-leasing arrangements (the CFS Dominion Energy template), or non-binding offtake terms—rather than firm capacity procurement until at least one independently verified net-electrical demonstration occurs (likely 2027–2029 window)

- Invest in interconnection and grid-forming inverter capabilities now. GFM inverter deployment, advanced power conditioning, and synchronous condenser planning have value across fusion, SMR, and renewable integration scenarios.

- Differentiate transmission-scale fusion (400+ MWe ARC-class) from genuinely distributed microreactors. Distribution-utility business cases for fusion microreactors remain speculative; transmission-utility cases are more credible by the early 2030s.

- Develop tritium-handling and radiological-waste competencies. Fusion plants will require licensed radiological staff, source-material handling, and Part 61–or-successor waste management contracts.

9.2 For National Governments and Regulators

- Resolve the mass-manufactured fusion machine licensing gap. The current U.S. framework is purpose-built for site-by-site licensing. Genuinely distributed fusion microreactors (analogous to Last Energy's PWR-5 or Radiant's Kaleidos approach in fission) require a categorical or design-certification pathway. NRC's pending report to Congress on this issue is a critical near-term deliverable.

- Address the lithium-6 strategic vulnerability. Re-establishing domestic enriched lithium 6 production, possibly through environmentally improved enrichment processes, warrants Defense Production Act Title III consideration in the U.S. and equivalent industrial-policy mechanisms in the EU.

- Secure tritium bridge supply. Government-backed offtake or strategic stockpile programs paralleling those for medical isotopes could de-risk early commercial fusion. The DOE-TVA Watts Bar lithium-control-rod tritium production model provides a precedent.

- Invest in the workforce. The NSF-funded Workforce Accelerator for Fusion Energy Development (Hampton, May 2024) identified a structural shortage of plasma physicists and fusion engineers. Targeted scholarship, visa, and apprenticeship programs are warranted.

- Coordinate internationally on TRL methodology and safeguards. The IAEA World Fusion Energy Group provides the appropriate forum; harmonized definitions reduce regulatory arbitrage and export-control friction.

- Avoid premature subsidy capture. The fusion industry's request for a $3 billion U.S. supplemental appropriation (FIA, 2024) and Europe's €10 billion ask should be evaluated against milestone-based delivery, not pre-paid in advance of demonstrations

9.3 For Institutional Investors

- Apply portfolio theory to fusion exposure. Across approaches (tokamak, FRC, MTF, stellarator, inertial), modal failure pathways differ; constructing an internally diversified fusion sleeve mitigates concept-specific risk. The 2024–2025 General Fusion experience illustrates idiosyncratic-failure risk even at well-capitalized companies

- Distinguish enabling-technology plays from end-product plays. Investments in HTS magnet manufacturing (TE Magnetics; commercial REBCO suppliers), tritium fuel-cycle technology (Kyoto Fusioneering; Fusion Fuel Cycles Inc.), and breeding-blanket materials may capture value across multiple end-state fusion architectures and have parallel applications in MRI, particle accelerators, and grid infrastructure.

- Stress-test valuations against extended timelines. The historical record (NIF, ITER, JET) suggests fusion timelines slip. Investment theses should accommodate 5-to-10-year delay scenarios without catastrophic NPV erosion.

- Watch for consolidation signals. With 53 companies and median additional capital requirements of ~$700 M, the FIA's own analysis implies unsustainable fragmentation. Late-2020s consolidation is a base-case expectation.

- Track regulatory milestones, not technical milestones, as risk inflection points. The October 2026 NRC final rule, the 2026 EU Fusion Strategy publication, and any Agreement State commercial-scale licensing decision are likely to repricing events.

10. References

Bragg-Sitton, S. M., et al. (2020). Integrated Energy Systems: 2020 Roadmap. Idaho National Laboratory, INL/EXT-20-57708

Clean Air Task Force. (2025, November). A Fusion Engine for Growth: A European Industrial Strategy for Fusion Energy. Brussels

Commonwealth Fusion Systems. (2024, December 17). Commonwealth Fusion Systems to Build World's First Commercial Fusion Power Plant in Virginia [Press release]. Devens, MA.

Commonwealth Fusion Systems. (2025, August 28). Commonwealth Fusion Systems Raises $863 Million Series B2 Round [Press release]. Devens, MA.

Fusion Industry Association. (2024). The Global Fusion Industry in 2024. Washington, DC.

Fusion Industry Association. (2025). The Global Fusion Industry in 2025. Washington, DC.

Fusion Industry Association. (2025). Fusion Industry Supply Chain Report 2025. Washington, DC.

International Atomic Energy Agency. (2023). IAEA World Fusion Outlook 2023. Vienna. https://doi.org/10.61092/iaea.ehyw-jq1g

International Atomic Energy Agency. (2024). Considerations of Technology Readiness Levels for Fusion Technology Components (IAEA-TECDOC-2047). Vienna.

International Atomic Energy Agency. (2025). IAEA World Fusion Outlook 2025. Vienna. https://doi.org/10.61092/iaea.agh6-zpih

Kuiken, T., & Offutt, M. C. (2025). Toward Commercial Fusion Energy: Considerations for Congress (CRS Report R48866). Congressional Research Service, Library of Congress.

National Academies of Sciences, Engineering, and Medicine. (2021). Bringing Fusion to the U.S. Grid. Washington, DC: The National Academies Press. https://doi.org/10.17226/25991

Nuclear Regulatory Commission. (2023, January 3). SECY-23-0001: Options for Licensing and Regulating Fusion Energy Systems. Washington, DC: U.S. NRC. ML22273A163.

Nuclear Regulatory Commission. (2023, April 13). Staff Requirements—SECY-23-0001—Options for Licensing and Regulating Fusion Energy Systems (SRM-SECY-23-0001). ML23103A449.

Nuclear Regulatory Commission. (2026, February 26). Regulatory Framework for Fusion Machines [Proposed Rule]. Federal Register, Docket ID NRC-2023-0071.

Pearson, R. J. (2022, June). The Availability and Supply of Critical Natural Resources for the Realization of a Fusion Pilot Plant: Fuels for Fusion. Presentation, U.S. DOE Fusion Workshop, Washington, DC.

Special Competitive Studies Project. (2025). Fusion Power: Enabling 21st Century American Dominance. Washington, DC

Tokamak Energy and the ST40 Team. (2024). Overview of recent results from the ST40 compact high-field spherical tokamak. Nuclear Fusion, 64(11). Published by IOP on behalf of the IAEA.

U.S. Department of Energy. (2022, March 17). Readout of the White House Summit on Developing a Bold Decadal Vision for Commercial Fusion Energy. Office of Science and Technology Policy.

U.S. Department of Energy. (2024). Fusion Energy Strategy 2024. Washington, DC.

Whyte, D., et al. (Commonwealth Fusion Systems and MIT Plasma Science and Fusion Center). (2024). High-temperature superconducting magnet papers (six-paper collection). IEEE Transactions on Applied Superconductivity.

Woodruff, S. (2024). A Costing Framework for Fusion Power Plants. arXiv:2601.21724.

Woodruff, S., et al. (2025). Extension of the Fusion Power Plant Costing Standard. arXiv:2602.19389. Clean Air Task Force International Working Group on Fusion Cost Analysis.

Wurzel, S. E., & Hsu, S. C. (2022). Progress toward fusion energy breakeven and gain as measured against the Lawson criterion. Physics of Plasmas, 29(6), 062103. https://doi.org/10.1063/5.0083990

Wurzel, S. E., & Hsu, S. C. (2025). Continuing progress toward fusion energy breakeven and gain as measured against the Lawson criteria. Physics of Plasmas, 32(11), 112106. https://doi.org/10.1063/5.0297357

Prepared April 2026. All projections, timelines, and LCOE estimates are subject to further validation. Where company- or industry-association-sourced data are cited, treat as self reported. Where regulatory deadlines are cited (e.g., NEIMA December 2027, NRC October 2026 f inal rule target), procedural delays are common in U.S. rulemaking and should not be treated as certain. The phrase "fusion microreactor" remains imprecisely defined in industry usage; readers should distinguish between transmission-connected sub-500 MWe plants (the dominant near term concept) and genuinely distributed sub-50 MWe units (which remain conceptual)